|

Why the total supply of stablecoins no longer tells you what crypto fears.

Stablecoin supply is no longer a fear gauge

Historically, a spike in stablecoin market caps meant traders were selling volatile crypto for safety. Today, an injection of capital into the stablecoin market might just be Visa, Stripe, or a corporate treasury using Circle to settle global payroll, actions disconnected from the price of leading cryptocurrencies. Tracking the total supply of stablecoins has lost its meaning as a market fear gauge. At the time, USDT and USDC looked interchangeable, a single pool of “safety” you could read as one number. The years since proved otherwise, and the clearest evidence is what the market actually did when it panicked.

2022: A flight from Tether, mistaken for a flight to safety

Every of 2022’s market corrections produced the same reflex. Traders fled Tether, the original stablecoin running since 2014, fearing its opaque reserves, and crowded into the younger USDC as the apparently safer dollar. The move was clean enough to pass for a fear signal: as Terra collapsed, USDC’s share of the two-coin market surged toward a peak near 45%. But it was never a flight to safety so much as a flight from one specific counterparty. The market was ranking perceived issuer risk, not finding shelter. That distinction stayed hidden until the supposed safe harbour broke too.

The SVB break that exposed both stablecoins

In March 2023, USDC’s own reserves were caught in the failure of Silicon Valley Bank and the coin briefly lost its peg, the haven breaking just as visibly as the dollar traders had fled. The lesson was uncomfortable. Regulated US banking risk was every bit as real as offshore counterparty risk, and structurally neither stablecoin was a haven. What had looked like a fear gauge was really a referendum on which issuer the market distrusted least that week. After SVB, the reflexive rotation into USDC simply stopped, and freed from that contest, the two coins began to drift apart.

Two coins that drifted into two destinies

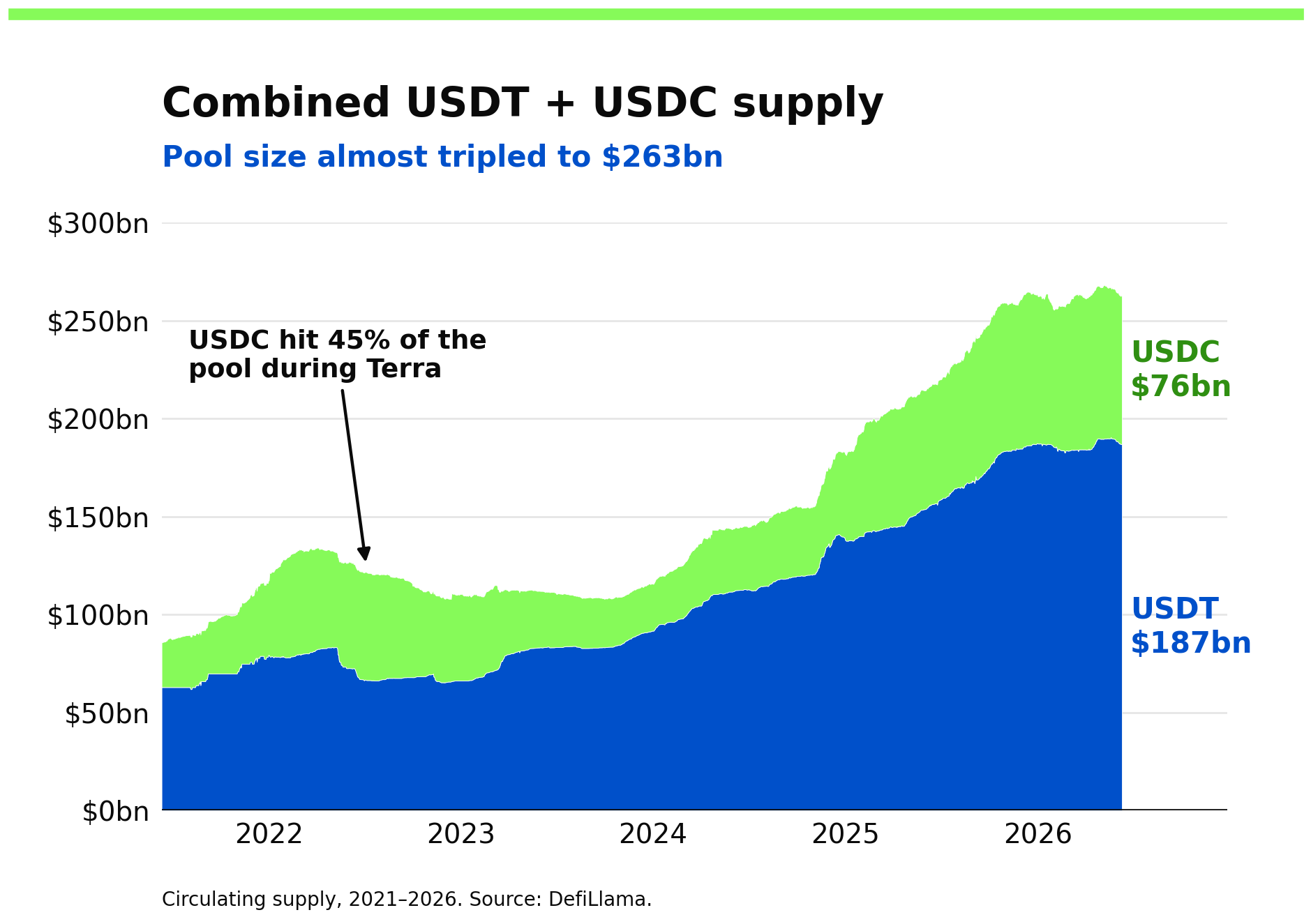

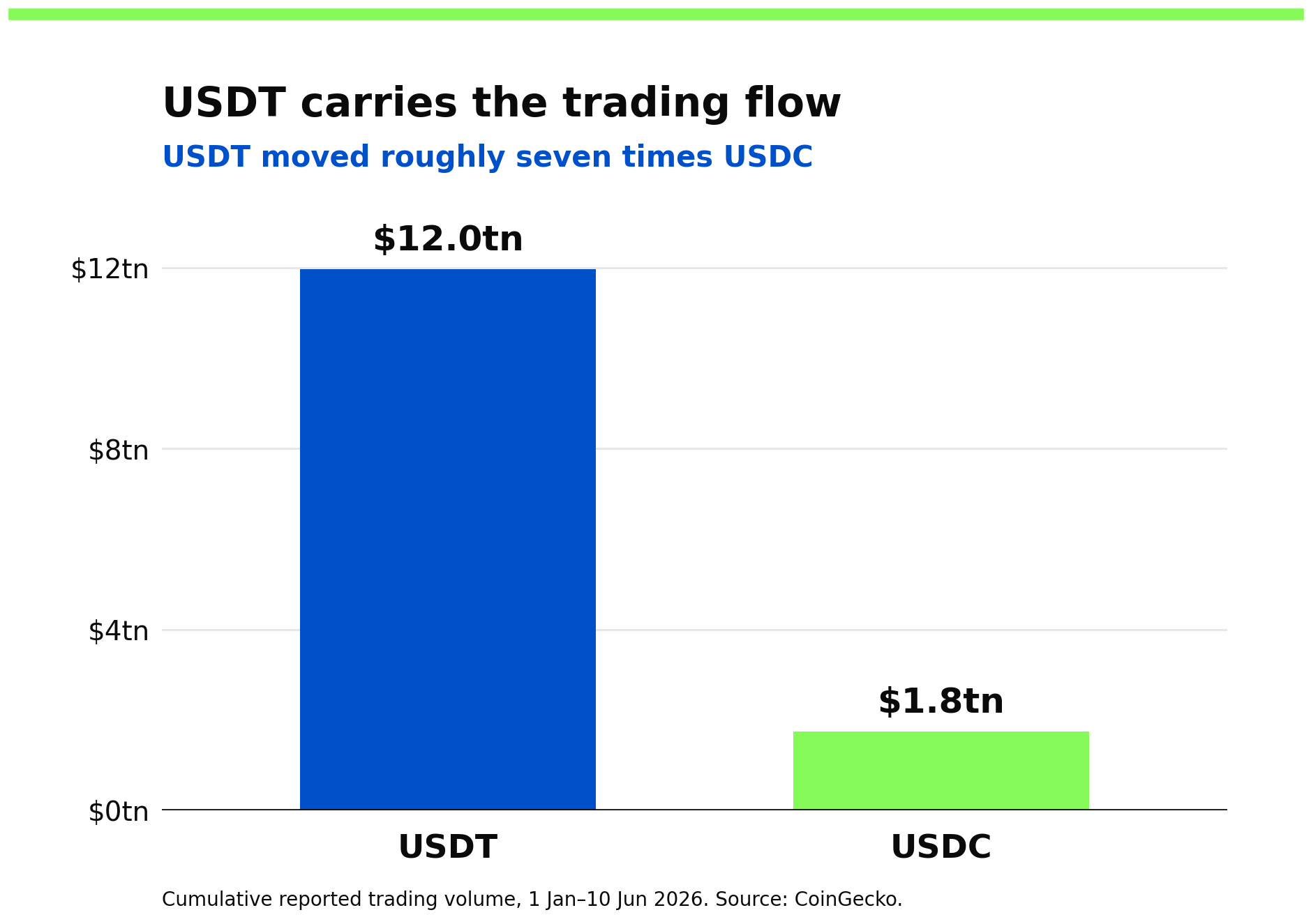

USDT became the stablecoin the trading world holds through a storm. Its supply grew from roughly $63bn to $187bn over five years, briefly overtaking Ethereum as the second-largest crypto asset in June 2026. USDC, live since 2018, moved onto compliant payment rails, settling remittances and B2B flows for the likes of Visa and Stripe. USDC was not left behind; it grew 73% in 2025 to $76bn. These two now compete for different users, subject to those users’ compliance requirements and regulatory regimes.

|

A combined supply of roughly $263bn does not sound large beside traditional money, but these are working dollars, not idle reserves: the default settlement layer for crypto trading and, increasingly, for payments and B2B flows. On adjusted measures, stablecoins now move value on a scale comparable to established payment networks, which is why both Tether and Circle have become infrastructure rather than instruments. The question is no longer how much dollar liquidity has entered crypto, but in the form of which stablecoin, and under whose rules.

The Compliance Gap: Will Regulation Fracture Global Stablecoins?

Both USDC and USDT remain the lifeblood of crypto. Yet they no longer compete for the same dollar; they serve entirely different financial systems. One is the compliant rail for European institutions; the other is the unbanked world’s liquidity layer. For anyone moving value on-chain, choosing a stablecoin is now a choice of jurisdiction, dictating which rules you accept, which venues you can access, and which counterparties will clear with you.

Yet this jurisdictional sorting threatens the ultimate promise of stablecoins: frictionless, borderless global settlement. The immediate challenge is bridging the gap between frameworks like Europe's MiCA and the US GENIUS Act. If these regimes cannot achieve regulatory interoperability, compliance will inevitably fragment the digital dollar by region.

Ensuring these frameworks talk to each other, rather than asset issuers creating more regional tokens, is the real work that will decide how far this infrastructure can actually reach.

|

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20295.5%20295.5'%20style='enable-background:new%200%200%20295.5%20295.5;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%23231F20;}%20%3c/style%3e%3ctitle%3eclock%20icon%3c/title%3e%3cpath%20class='st0'%20d='M268.8,147.7c0,66.9-54.2,121.1-121.1,121.1c-66.9,0-121.1-54.2-121.1-121.1S80.9,26.6,147.8,26.6V0%20C66.1,0,0,66.1,0,147.8s66.1,147.8,147.8,147.8s147.8-66.1,147.8-147.8c0,0,0,0,0,0H268.8z'/%3e%3cpolygon%20class='st0'%20points='134.4,80.6%20134.4,134.4%20134.4,147.8%20134.4,161.1%20187.8,161.1%20187.8,134.4%20161.1,134.4%20161.1,80.6%20'/%3e%3c/svg%3e) 5 min read

5 min read