THE TRUE VALUE OF SECURITY TOKENS LIES IN THEIR PROOF OF OWNERSHIP

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20295.5%20295.5'%20style='enable-background:new%200%200%20295.5%20295.5;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%23231F20;}%20%3c/style%3e%3ctitle%3eclock%20icon%3c/title%3e%3cpath%20class='st0'%20d='M268.8,147.7c0,66.9-54.2,121.1-121.1,121.1c-66.9,0-121.1-54.2-121.1-121.1S80.9,26.6,147.8,26.6V0%20C66.1,0,0,66.1,0,147.8s66.1,147.8,147.8,147.8s147.8-66.1,147.8-147.8c0,0,0,0,0,0H268.8z'/%3e%3cpolygon%20class='st0'%20points='134.4,80.6%20134.4,134.4%20134.4,147.8%20134.4,161.1%20187.8,161.1%20187.8,134.4%20161.1,134.4%20161.1,80.6%20'/%3e%3c/svg%3e) 3 min read

3 min readOriginally published on 12 AUG 2020, updated on 06 FEB 2026.

1. THE TOKENIZATION (R)EVOLUTION

"Every stock, every bond, every fund—every asset—can be tokenized. If they are, it will revolutionize investing."¹

These words from Larry Fink, CEO of BlackRock—the world's largest asset manager with over $11 trillion under management—signal a fundamental shift in how global financial markets will operate. In December 2025, Fink and BlackRock COO Rob Goldstein described tokenization as potentially triggering finance's biggest transformation since the 1970s, comparing its impact to the rise of the early internet.²

The institutional momentum is unmistakable. BlackRock's BUIDL tokenized fund reached nearly $3 billion in assets in 2025. Franklin Templeton launched the first fully tokenized UCITS fund in Luxembourg in 2024, followed by expansions to Hong Kong and Singapore in 2025.³ The Financial Stability Board, IOSCO, and the OECD have all published major reports analyzing tokenization's implications for financial markets.⁴

The benefits driving institutional adoption are clear: automated collateral management, 24/7 settlement, enhanced capital efficiency, reduced counterparty risk, and programmable compliance. As Fink noted, "Markets wouldn't need to close. Transactions that currently take days would clear in seconds."

This article examines how Luxembourg law—one of the world's leading fund jurisdictions—accommodates this transformation, and why registered securities (titres nominatifs) remain the optimal legal form for issuers and investors seeking the full benefits of tokenization.

¹ Larry Fink, 2025 Annual Chairman's Letter to Investors, BlackRock (March 2025).

² Larry Fink and Rob Goldstein, "Tokenization could do for finance what the early internet did for information", The Economist, December 2025.

³ Franklin Templeton launched the Franklin OnChain U.S. Government Money Fund as the first Luxembourg-domiciled fully tokenized UCITS product in February 2025, using its proprietary Benji Technology Platform on the Stellar blockchain. See Franklin Templeton press release, 19 February 2025.

⁴ FSB, The Financial Stability Implications of Tokenisation, October 2024; IOSCO, Tokenization of Financial Assets, November 2025; OECD, Tokenisation of Assets and Distributed Ledger Technologies in Financial Markets, January 2025.

2. THE CONCEPT OF SECURITIES

"The written does not create the right - it proves it" ("L'écrit ne crée pas le droit, il le constate") observed French legal academic François-Xavier Lucas when analysing the transfer of securities.⁵

The main idea behind this statement is to highlight that the rights someone owns exist independent of having them written down. However, in order to prove to any third party (inter omnes) the ownership of these rights, a layer of trust is required.

Historically, securities (in French "titres") were created for that exact purpose. Securities represent an underlying value by abstracting it into an instrument ("instrumentum") in order to establish trust vis-à-vis any other person that the holder is actually the rightful owner of the rights.

While German law implies in the terms "Wertpapier" and "Verbriefung" that rights need to be put down on paper, French law—and by extension Luxembourg law—incorporated a more abstract understanding using the terms "titres" and "titrisation". This article argues that the main purpose of securities in Luxembourg is simply to make a right ownable and transferable.

The different forms of securities distinguish themselves mainly by setting different rules on how securities are created and made transferable. The creation concept refers to how rights issued by an entity are made ownable by the receiver. The transferability concept concerns how the underlying rights can be transferred to a third party.

For capital markets, negotiability is critical. Negotiability ensures that rights are valid not only between transacting parties ("inter partes") but also vis-à-vis third parties including the issuer ("inter omnes"). This requires that acquirers are protected against claims from former owners—otherwise securities would be useless for secondary markets.

2.1 Three Forms of Securities under Luxembourg Law

Luxembourg law recognizes three forms of securities:

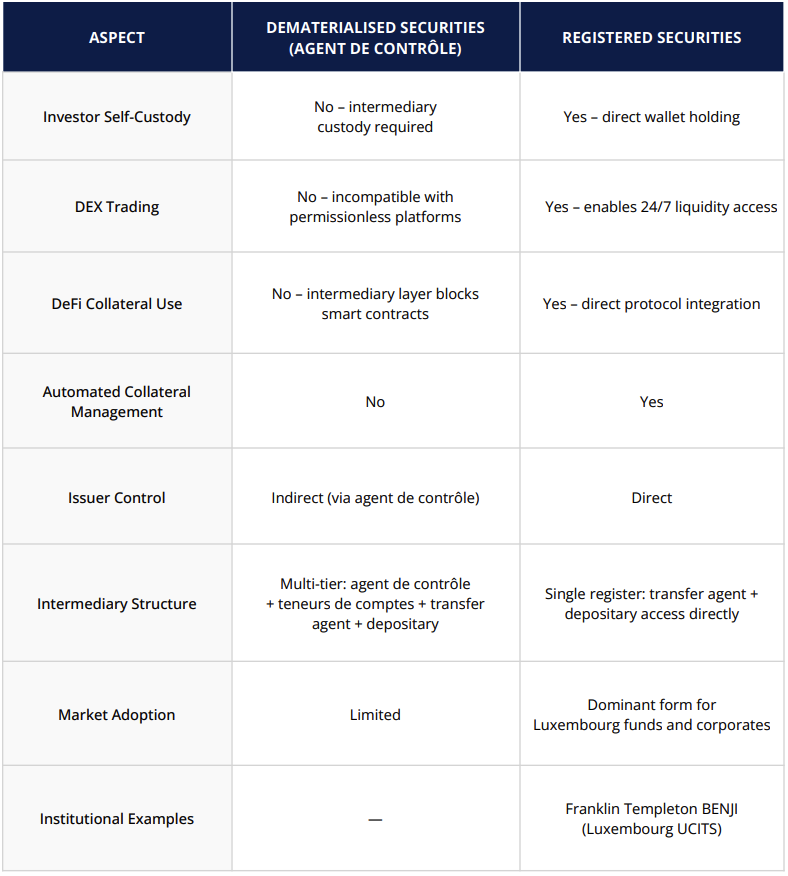

Bearer Securities (titres au porteur): These are created by materialising the underlying rights, historically by printing a paper certificate. Transfer occurred through physical handover. However, since the Luxembourg law on immobilisation of bearer shares, bearer securities must be deposited with a depositary who maintains a register. The issuer is not in control of the register and requires an intermediary, making this form less suitable for blockchain-based tokenization.

Dematerialised Securities (titres dématérialisés): Introduced by the law of 6 April 2013, these are created through a clearing institution or central securities depository who enter securities directly in a securities account ("compte-titres"). Transfer occurs by book-entry between accounts maintained by security depositories. Negotiability is ensured by trust in the book entry. The 2024 amendments have expanded this regime to include the agent de contrôle option, discussed in Section 3.

Registered Securities (titres nominatifs): These are created by the issuer through opening a register of security holders. Crucially, this register can be held by the issuing company itself. Transfer occurs by inscribing the acquirer in the register, with the underlying right assigned per Article 1690 of the Luxembourg civil code. Negotiability is ensured by the fact that a prior deficient registration does not affect the bona fide acquirer—in Luxembourg, as in French law, acquirers are protected against claims from former right holders if they had no knowledge of any deficiency.⁶

For tokenization, the critical question is: which form enables the full benefits that institutions seek—direct custody, smart contract composability, DEX liquidity, and automated collateral management?

⁵ François-Xavier Lucas, "Les transferts temporaires de valeurs mobilières", LGDJ, 1997.

⁶ Contrary to German law where the acquirer would not obtain the right against the issuer if the seller assigned a security they did not own (kein gutgläubiger Erwerb bei Abtretung von Rechten gem. §§ 398ff BGB).

3. THE 2024 BLOCKCHAIN LAW AMENDMENTS

3.1 Recognition of Distributed Ledger Technology

The Luxembourg legislator has demonstrated commitment to financial innovation through amendments to the law of 6 April 2013 on dematerialised securities. These amendments introduce the "agent de contrôle" (control agent) as a new option for holding the issuance account, with explicit recognition that such accounts "may be held and securities entries may be made within or through secure electronic recording devices, including distributed electronic registers or databases."⁷

The agent de contrôle must be an investment firm, credit institution, or settlement system designated by the issuer, responsible for maintaining the issuance account on DLT, monitoring the custody chain, and verifying reconciliation between the issuance account and investor securities accounts.⁸

3.2 The Custody Structure Challenge

However, a critical examination of the dematerialised securities regime reveals a structural limitation that affects both issuers and investors seeking the transformative benefits of tokenization.

Under this regime, securities must legally exist as entries in securities accounts (comptes-titres) maintained by authorized account holders (teneurs de comptes).⁹ This creates a mandatory two-tier structure: the agent de contrôle at the issuer level, and separate regulated account holders maintaining securities accounts for investors.

The fundamental consequence: investors cannot hold tokens directly in their own wallets. The tokens representing their holdings must legally reside in a securities account maintained by an authorized intermediary—even where the underlying infrastructure uses blockchain technology.

This has profound implications:

DEX Trading: Decentralised exchanges operate on the premise that users trade directly from self-custodied wallets. Since dematerialised securities cannot legally exist outside intermediary-maintained accounts, they cannot access permissionless DEX platforms or 24/7 global liquidity pools.¹⁰

DeFi Collateral: The inability for investors to hold tokens directly prevents use as collateral in DeFi lending protocols or integration with automated collateral management systems—precisely the capabilities driving institutional interest in tokenization.¹¹

Intermediary Duplication: For regulated fund structures, the agent de contrôle model does not replace existing transfer agent and depositary requirements under Luxembourg fund law—it adds layers on top of them, resulting in increased costs rather than the streamlined operations institutions seek.¹²

⁷ Art. 1(1bis) of the amended Loi du 6 avril 2013 relative aux titres dématérialisés.

⁸ Art. 1(10bis) of the amended law defines the agent de contrôle's functions and Art. 21bis establishes governance and notification requirements.

⁹ Art. 2(1) of the amended law: "Les titres dématérialisés ne sont représentés que par une inscription en compte-titres."

¹⁰ Transfer of dematerialised securities occurs by book-entry between securities accounts per the Law of 1 August 2001 on the circulation of securities.

¹¹ Institutional tokenization is increasingly driven by operational efficiencies: automated collateral management can reduce margin calls and optimize capital deployment in real-time—capabilities requiring direct smart contract interaction.

¹² Under Luxembourg fund law (Law of 17 December 2010 and Law of 12 July 2013), regulated funds must appoint depositaries and typically engage transfer agents regardless of the securities form used.

4. REGISTERED SECURITIES: THE INSTITUTIONAL CHOICE

4.1 Direct Issuer-Investor Relationship

Registered securities are created by the issuer through the opening of a register of security holders. Unlike dematerialised securities, this register can be held by the issuing company itself, creating a direct legal relationship between issuer and investor without mandatory intermediaries.¹³

The vast majority of Luxembourg investment funds and corporate issuers use registered securities. This is not coincidental—the form provides flexibility, direct control, and proven legal certainty.

4.2 Franklin Templeton's Approach

Notably, Franklin Templeton's Luxembourg-domiciled tokenized UCITS fund uses its proprietary Benji Technology Platform as a blockchain-integrated transfer agency, maintaining direct records of share ownership on public blockchains.¹⁴ The structure demonstrates that institutional-grade tokenization can be achieved through registered securities frameworks, with the transfer agent accessing and maintaining the blockchain-based register directly.

This approach delivers the benefits of blockchain—transparency, immutability, efficiency—while maintaining compliance with fund regulations. The transfer agent and depositary fulfill their supervisory roles by interfacing directly with the token register, rather than through additional intermediary layers.

4.3 Advantages for Tokenization

Investor Self-Custody: Tokens representing registered securities can be held directly in investor wallets—whether personal wallets or institutional custody solutions with direct blockchain access. This is the foundational requirement for accessing DeFi functionality.

DEX and Secondary Market Access: With tokens held directly in investor wallets, registered securities can be traded on decentralised exchanges, providing access to 24/7 global liquidity and automated market making.

DeFi Composability: Self-custodied tokens can interact directly with smart contracts, enabling use as collateral in lending protocols, participation in liquidity pools, and integration with automated collateral management systems.

Streamlined Regulatory Compliance: Transfer agents and depositaries can directly access blockchain-based registers to fulfill their regulatory duties under fund law. The blockchain provides an immutable audit trail that enhances—rather than complicates—supervisory functions.¹⁵

Programmable Distributions: Dividends, interest, and redemptions can be executed directly by the issuer via smart contracts, enabling automation and reduced operational costs.

¹³ See Articles 430-3 and 430-4 of the Law of 10 August 1915 on commercial companies.

¹⁴ Franklin Templeton press release, 19 February 2025: "Franklin OnChain U.S. Government Money Fund represents the first Luxembourg domiciled fully tokenised UCITS product. It is launched on public blockchain Stellar, using the firm's proprietary inhouse blockchain-enabled transfer agency platform."

¹⁵ The blockchain-based register provides transfer agents and depositaries with real-time, immutable access to investor holdings, transaction history, and compliance data.

5. RECOMMENDED CLARIFICATIONS

While registered securities under Luxembourg law are already well-suited for tokenization, explicit recognition of DLT—mirroring the language now found in the dematerialised securities law—would provide additional legal certainty.

This article suggests adding the following clarifications to Articles 430-3 and 430-4 of the Luxembourg corporate law:

"Art. 430-3 (addition)

La société peut tenir le registre et effectuer les inscriptions de titres dans le registre au sein ou par le biais de dispositifs d'enregistrement électroniques sécurisés tels que registres ou bases de données électroniques distribués."

"Art. 430-4 (addition)

Il est loisible à la société d'accepter et d'inscrire sur le registre un transfert qui serait constaté par la correspondance ou d'autres documents établissant l'accord du cédant et du cessionnaire y compris par le biais de dispositifs d'enregistrement électroniques sécurisés tels que registres ou bases de données électroniques distribués."

6. COMPARATIVE OVERVIEW

SUMMARY

Luxembourg law provides a robust foundation for the tokenization revolution that leading institutional players are driving. The 2024 amendments to the dematerialised securities law demonstrate the legislator's commitment to financial innovation and explicit recognition of distributed ledger technology.

However, for issuers and investors seeking the full transformative benefits of tokenization—direct custody, DEX access, DeFi composability, automated collateral management, and streamlined operations—registered securities remain the optimal choice under Luxembourg law.

The registered securities model enables what the institutional market demands: a direct relationship between issuer and investor, self-custody capability for token holders, and seamless integration with the broader decentralised finance ecosystem. Transfer agents and depositaries can fulfill their regulatory functions by accessing a single blockchain-based register directly, achieving compliance without intermediary duplication.

As Larry Fink observed, tokenization represents the next major evolution in market infrastructure. Luxembourg's flexible legal framework—particularly its established registered securities regime—positions the jurisdiction to accommodate this transformation while maintaining the regulatory rigor that institutional investors expect.

To download the full analysis CLICK HERE.

BY TOBIAS SEIDL

Discover related insights

STOKR UPDATE - FEBRUARY 2026

STOKR starts 2026 with key milestones including rwa.xyz integration, the launch of the Goldstream Fund, and a first look at our upcoming brand film.

STOKR Secures CASP and PI Licences in Luxembourg