STRC: The Ecosystem, The Patterns, The Outlook

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20295.5%20295.5'%20style='enable-background:new%200%200%20295.5%20295.5;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%23231F20;}%20%3c/style%3e%3ctitle%3eclock%20icon%3c/title%3e%3cpath%20class='st0'%20d='M268.8,147.7c0,66.9-54.2,121.1-121.1,121.1c-66.9,0-121.1-54.2-121.1-121.1S80.9,26.6,147.8,26.6V0%20C66.1,0,0,66.1,0,147.8s66.1,147.8,147.8,147.8s147.8-66.1,147.8-147.8c0,0,0,0,0,0H268.8z'/%3e%3cpolygon%20class='st0'%20points='134.4,80.6%20134.4,134.4%20134.4,147.8%20134.4,161.1%20187.8,161.1%20187.8,134.4%20161.1,134.4%20161.1,80.6%20'/%3e%3c/svg%3e) 6 min read

6 min readPART 2 — WHAT IS BEING BUILT ON TOP, AND WHAT IT MEANS

Download the full report here.

In Part 1 we walked through STRC itself: an $10.5bn variable-rate perpetual preferred paying 11.5% in monthly cash, with ROC tax treatment that lifts the effective yield for taxable US holders. We separated the two ATM flows (the STRC ATM that buys Bitcoin, and the MSTR common ATM that fills the $1.44bn USD Reserve which pays the dividend) and showed how they close into a single engine through the Bitcoin balance sheet. We named the three pressure points (par-peg, mNAV, cash buffer), watched the engine stall in Q1 2026, and noted the structure survived because of design and because investors stayed convinced. In Part 2 we step back from the instrument and look at the ecosystem that has formed around it in under twelve months.

WHAT IS BEING BUILT ON TOP OF DIGITAL CREDIT

Other issuers replicating the preferred structure. Strive (NASDAQ: ASST) launched SATA, a US variable-rate perpetual preferred at 13.0% with the same monthly rate-adjustment mechanism and the same ROC tax treatment that STRC offers. As of May 2026 Strive holds ~15,000 BTC and ~$50m of STRC itself, making it simultaneously an issuer of the model and a buyer of the original. Metaplanet (TSE: 3350) raised $150m in November 2025 through MERCURY, a fixed-rate 4.9% convertible perpetual preferred denominated in yen and junior to its MARS Class A. The replication wave has crossed continents.

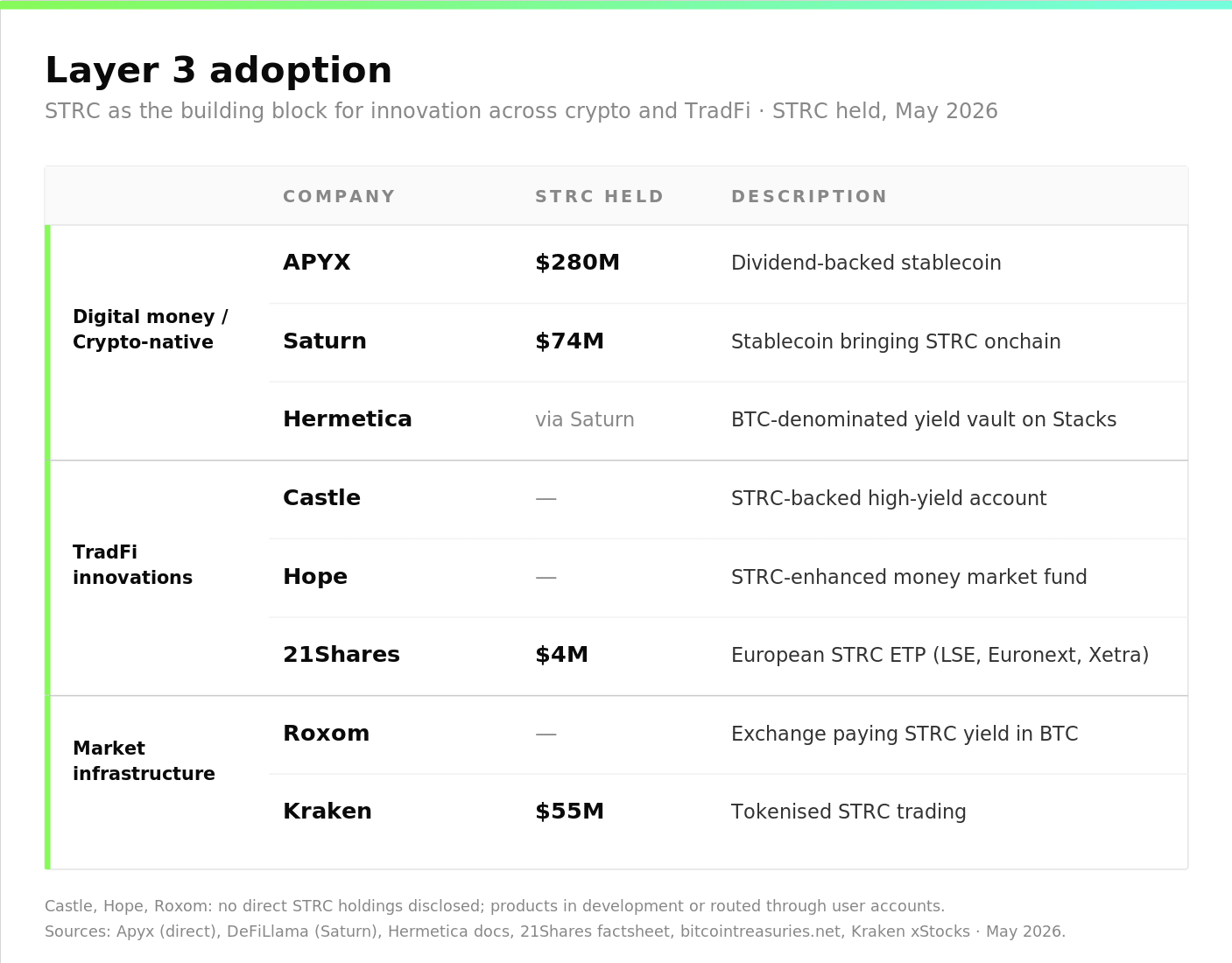

Conventional wrappers. Ondo Finance issued a tokenised STRC-tracking note on Ethereum, BNB Chain and Solana through a BVI vehicle. 21Shares offers a European exchange-traded product. Most consequentially, BlackRock's PFF ($13bn+ AUM) holds approximately $210m of STRC as a passive index position, plus another ~$170m in STRF and STRD. STRC has entered mainstream institutional fixed-income infrastructure not as a discretionary allocation but as an index-weight consequence of its market capitalisation.

DeFi infrastructure on the dividend stream. Saturn issues sUSDat, an on-chain wrapper for STRC's dividend cash flows. Pendle V2 splits sUSDat into Principal and Yield tokens. Strata layers tranched credit on top (senior srUSDat at ~7%, junior jrUSDat at ~13%). Morpho and other DeFi money markets accept the wrappers as collateral. Approximately $200m of STRC has been tokenised, with around $100m actively trading on Pendle.

Carry trades, collateralised lending, and exchange use. Beyond the named protocols, STRC is appearing in less visible places. Funds are running carry trades that pair long STRC against lower-yielding fixed-income instruments to harvest the spread. Exchanges have started accepting STRC as margin collateral, allowing holders to borrow stables or BTC against their position without selling the dividend stream. STRC notes (wrapped representations of STRC suitable for on-chain settlement) are beginning to circulate, with margin-lending facilities on selected venues. These uses do not show up in tokenisation TVL or in PFF holdings, but they collectively turn STRC into something closer to a base-rate instrument for credit strategies in and around Bitcoin.

One useful lens. The ecosystem fans out along a spectrum. At one end sit products that keep STRC exposure inside conventional issuer infrastructure (SATA, MERCURY, DGCR if approved, the UTXO LP). In the middle sit wrappers that move the exposure onto traditional listed-securities rails for new audiences (21Shares, PFF). At the far end sit products that move the exposure into fully peer-to-peer composable formats on chain (Saturn, Pendle, Strata, Morpho). Each step toward the composable end buys interoperability with other DeFi protocols at the cost of adding new risk surfaces: wrapper risk, smart-contract risk, liquidation risk under stress. The further from the corporate issuer, the less of STRC's actual mechanism survives, and the more the product is exposed to STRC's secondary market price rather than the engineered stated value.

THREE PATTERNS WORTH NAMING

Audience segmentation. Every builder usually is optimisessing for one target investor base. SATA, DGCR and UTXO target US institutional. MERCURY targets Asian institutional. Ondo and the DeFi stack target DeFi-native. 21Shares targets European retail. PFF is the passive default for mainstream US fixed income. The category will grow as a portfolio of products, not as one converging design.

Category formalisation. Three issuers and a US ETF filing now use “digital credit” as a defined category. Naming precedes indexation. Indexation precedes allocation. The speed of this is unusual: STRC launched July 2025, and by May 2026 a SEC-filed ETF and an institutional LP both explicitly carry the category in their names.

Composability has a cost, and the par-peg only survives at one end. STRC's monthly rate-adjustment is a discretionary issuer action: the company looks at the market price and realigns the rate to keep STRC near par. Distribution to DeFi requires fungibility (tokens that behave identically across protocols), and that fungibility is incompatible with a rate that can be realigned each month. The more distributed the wrapper, the less of STRC's mechanism actually survives, and the more the product is exposed to STRC's secondary market price rather than to the engineered par. That is not a flaw of the wrappers; it is the structural cost of moving exposure into peer-to-peer composability. It also means the failure mode at the DeFi end of the ecosystem will look different from the failure mode at the corporate-issuer end.

THE ECOSYSTEM IN CONTEXT: SMALL INSIDE TRADFI, FOUNDATIONAL FOR WHAT COMES NEXT

Size first. STRC is the largest tradable preferred listed in the US. The ecosystem built on top of it (tokenised wrappers, tranched credit, carry trades, exchange collateral) totals at most a few hundred million dollars of active TVL plus a similar amount of opaque off-chain positioning. That is meaningful inside crypto and meaningful for STRC's secondary-market behaviour. It is small in absolute terms compared to the trillions of dollars sitting in conventional preferred-stock, investment-grade credit and money-market funds.

What that scale gap implies. Any market distortion that originates inside the STRC ecosystem (a looping trade unwinding under stress, a tranche getting liquidated noisily, a wrapper depegging) is bound by the TradFi capital that stands ready to step in at attractive prices. A flash crash in a Pendle yield token or a Strata tranche is, from the perspective of a TradFi credit desk, a buying opportunity in a security whose underlying still pays an 11.5% monthly cash dividend backed by 843,738 BTC. The arbitrage mechanism is asymmetric: TradFi can scale into mispricings; the DeFi ecosystem cannot scale out of them at the same pace. That asymmetry caps how systemic the failure modes can become.

The product implication. STRC provides a stable TradFi-anchored foundation. The applications being built on top (wrappers, tranches, lending, carry) are the early stages of a credit market that will mature alongside the underlying. As long as STRC's par-peg holds and Strategy continues to honour the dividend, these applications inherit a high-quality base rate. When (not if) one of the DeFi stacks fails noisily, the failure will look like a crypto incident even though the underlying STRC will keep paying its dividend on schedule. Operators building in this space need to design with that asymmetry in mind.

OUTLOOK

Three forward signals are worth watching. The first is the shareholder vote on moving STRC to semi-monthly distributions; if it passes, the ex-dividend recovery window shrinks and the STRC ATM can issue more continuously, which improves accumulation efficiency without adding leverage. The second is institutional adoption: PFF's passive inclusion has been the cleanest mainstream allocation channel so far, and additional preferred-stock ETFs will likely follow as indices update their methodologies to reflect STRC's market cap. The third is replication: SATA and MERCURY have demonstrated that the structure ports across issuers and jurisdictions, and a European or UK equivalent is now the most obvious open seat.

Put together, the most likely trajectory for the next twelve months is more, not less, of the same. More issuers carrying the category name. More wrappers giving different audiences different shapes of the same exposure. More DeFi infrastructure layering on top of STRC's yield. More institutional allocation through index inclusion rather than discretionary mandate. The interesting innovation is not whether something dramatic breaks; it is how the credit market that has formed around Bitcoin matures from a single instrument into a working category. STRC was the first scale instance. It is unlikely to be the last.

Download full report here.

Patrick Lehner

Financial Analyst