|

STOKR Insights

|

|

Tokenisation, Bitcoin infrastructure, and capital markets; Bi-weekly intelligence from STOKR.

|

|

|

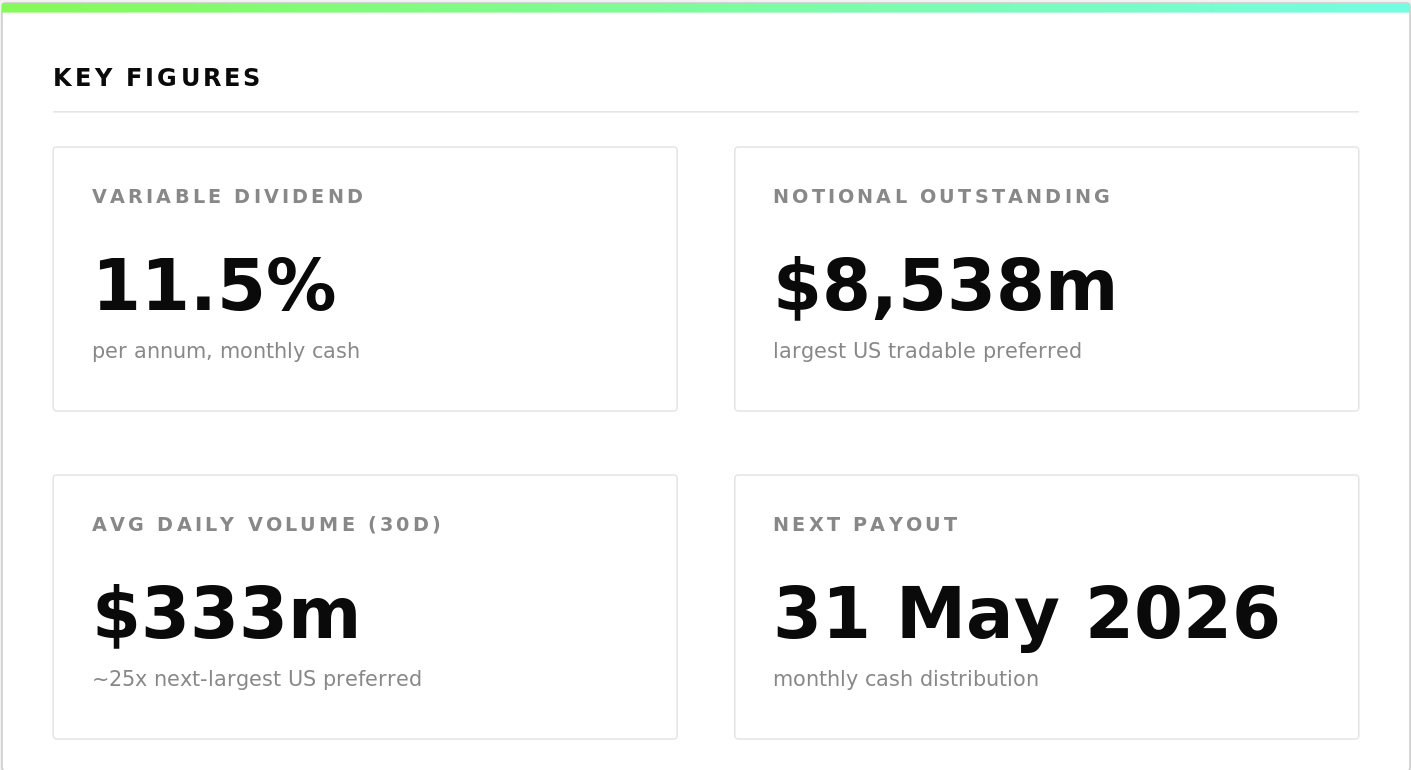

Of all the financial engineering Strategy has shipped over five years (common-stock ATMs, convertible debt, four perpetual preferred series), one instrument has pulled ahead. STRC, Strategy’s variable-rate perpetual preferred, has reached $8.5bn outstanding in under nine months. It is the largest tradable preferred listed in the US, roughly 25x more liquid than the next-largest US preferred, and in four months of 2026 has financed close to 77,000 BTC purchases, about ten times the spot Bitcoin ETF total. Strategy calls it digital credit. From a market-structure perspective, it is the fastest horse in the stack.

|

|

|

|

STOKR just published two research notes examining this structure in depth: the mechanics of the ATM cycle, the tax treatment, and what the emerging digital credit category means for institutional capital allocation. This week’s newsletter covers the key concepts and figures; the two articles are where the full analysis lives.

|

|

|

|

|

|

|

|

|

|

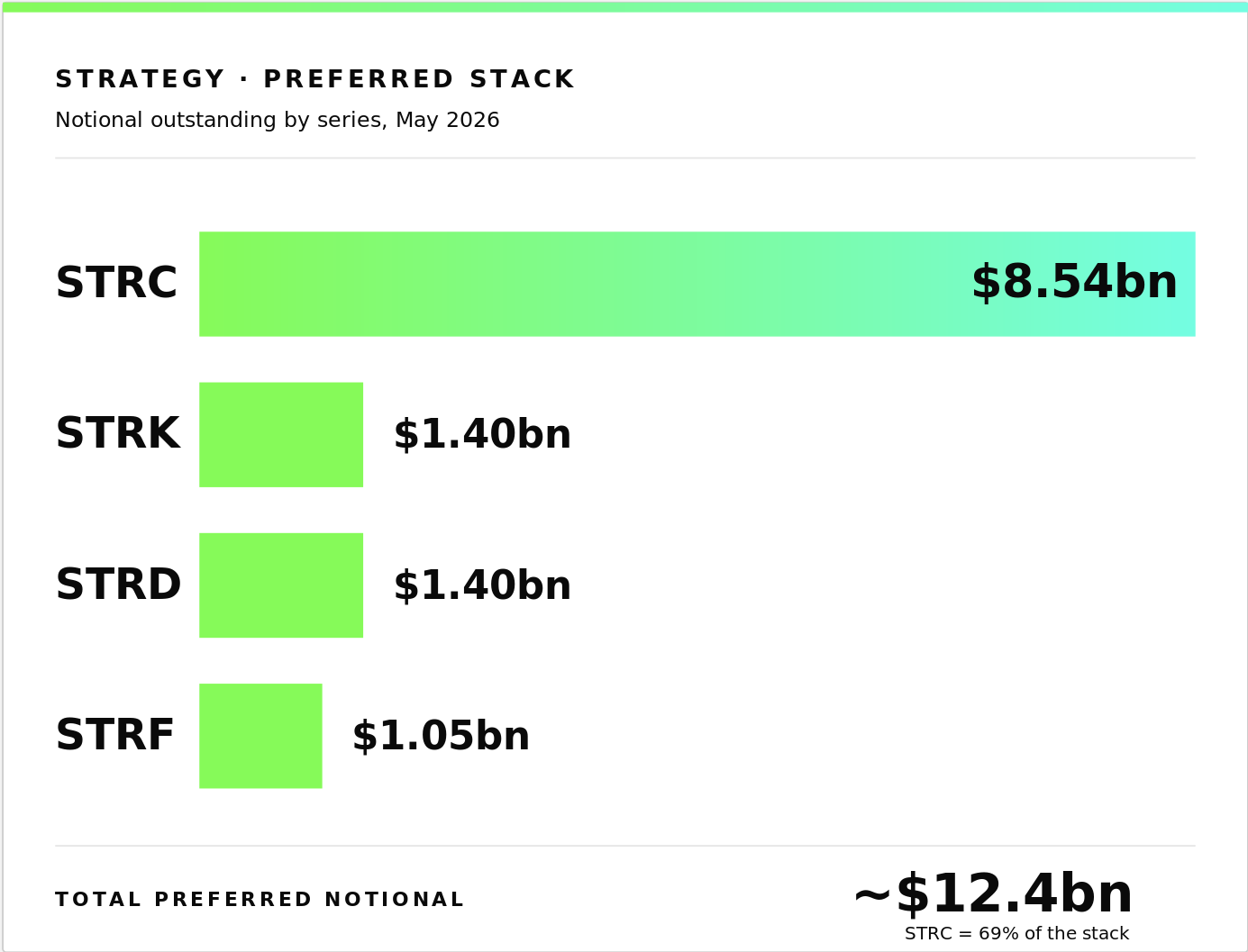

STRC pays a monthly cash distribution at an annualised rate of 11.5%, has a $100 stated amount, and Strategy may adjust the rate each month at its discretion to keep the price near par. The product sits in Strategy’s preferred stack alongside STRF, STRK and STRD; together the four series total roughly $12.4bn in notional, with STRC alone accounting for about 69%. Each series has its own at-the-market (ATM) programme, and STRC’s has done the heavy lifting in 2026.

|

|

The design feature most investors miss

|

|

|

STRC’s headline rate of 11.5% is not what makes it interesting. 100% of 2025 distributions were classified as Return of Capital (ROC) for US federal tax purposes. The distribution is treated as a return of the holder’s own invested capital rather than as taxable dividend income: tax is deferred (and basis-reduced) rather than paid in the year the cash arrives. For a taxable US investor, that turns the 11.5% gross into a materially higher after-tax yield than a comparable taxable dividend. Strategy expects ROC treatment to continue for the foreseeable future.

|

|

|

|

The deeper question is not what STRC does. It is how the dividend gets paid. Strategy’s software business doesn’t cover the bill, and Strategy says it will not normally sell Bitcoin to do so. The cash comes from two at-the-market programmes running in parallel: the STRC ATM buys Bitcoin, the MSTR common ATM fills the $2.25bn USD Reserve that pays the distributions. The two pipes close through the Bitcoin balance sheet itself, and the cycle is what makes the structure work.

|

|

A category, named and forming

|

|

|

Strategy frames STRC as the first scale instance of digital credit: credit products built on a Bitcoin balance sheet. The label is settling. Strive’s SATA replicates the model in the US, albeit shifting from monthly to daily dividend payments. Metaplanet’s MERCURY in Japan, and Strive and Tuttle have filed for DGCR, the first ETF explicitly built around the category. As the category matures, STRC’s variable rate is starting to look like a de facto base rate for the products built on top.

|

|

|

|

Part 1 walks through the instrument and the engine: how the two ATM programmes interact, what the Q1 2026 stress test revealed about the structure’s breaking points, and why the USD Reserve was the design choice that mattered. Part 2 maps the ecosystem now forming on top of STRC, the patterns inside it, and the outlook for the digital credit category.

|

|

|

|

|

|

STOKR S.A.

|

stokr.io

|

|

STOKR is a brand name. The main operations are conducted by STOKR S.A., a public limited company (société anonyme) incorporated in Luxembourg, with its registered office at 9, rue du Laboratoire, L-1911 Luxembourg. The company is registered with the Luxembourg Register of Commerce and Companies under number B226662, holds business license number 10098697/1, and is registered for VAT under number LU31077475. STOKR S.A. is registered as a virtual asset service provider (VASP) with the Luxembourg financial regulator, the Commission de Surveillance du Secteur Financier (CSSF). This communication is for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any financial instruments or digital assets.

|

|

|

|

|

%20--%3e%3csvg%20version='1.1'%20id='Layer_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%20295.5%20295.5'%20style='enable-background:new%200%200%20295.5%20295.5;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:%23231F20;}%20%3c/style%3e%3ctitle%3eclock%20icon%3c/title%3e%3cpath%20class='st0'%20d='M268.8,147.7c0,66.9-54.2,121.1-121.1,121.1c-66.9,0-121.1-54.2-121.1-121.1S80.9,26.6,147.8,26.6V0%20C66.1,0,0,66.1,0,147.8s66.1,147.8,147.8,147.8s147.8-66.1,147.8-147.8c0,0,0,0,0,0H268.8z'/%3e%3cpolygon%20class='st0'%20points='134.4,80.6%20134.4,134.4%20134.4,147.8%20134.4,161.1%20187.8,161.1%20187.8,134.4%20161.1,134.4%20161.1,80.6%20'/%3e%3c/svg%3e) 5 min read

5 min read